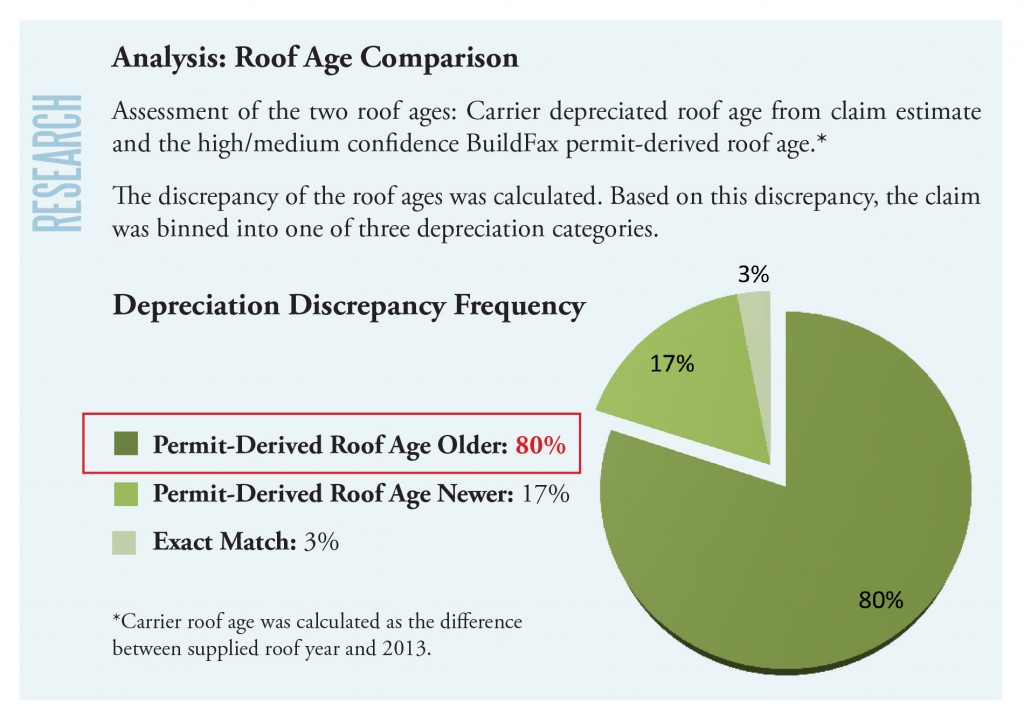

When a claims adjuster looks at a roof he will consider the condition of the roof as well as its age.

Roof depreciation life.

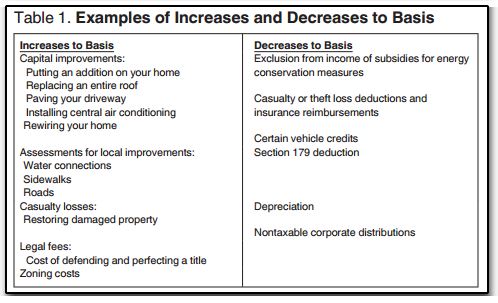

Decide if the new roof is a capital improvement.

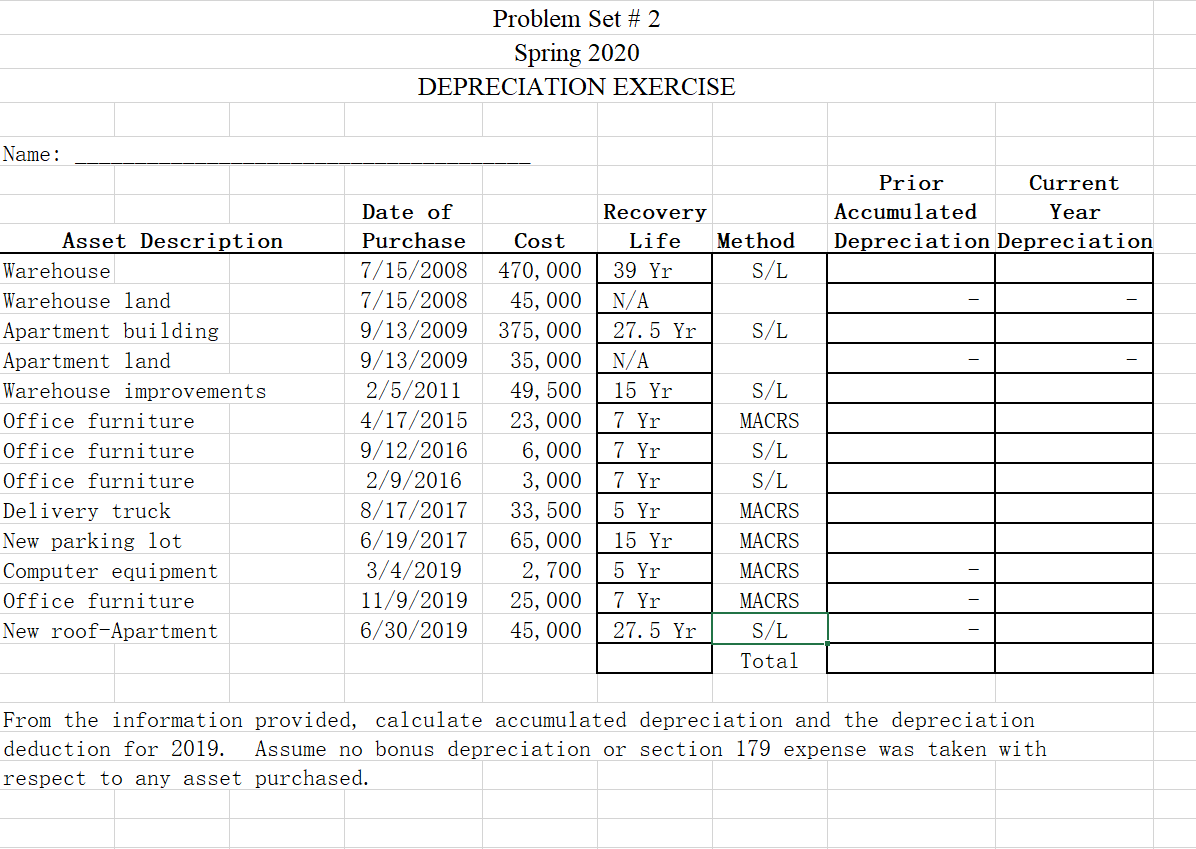

For example if you ve owned a rental property for 10 years before you installed a new roof you can depreciate the roof over 27 5 years even though you have 17 years of depreciation left on the property.

Calculating depreciation based on age is straightforward.

If improved materials were used taxpayers would need to focus on the expected life of the old roof versus the expected life of the new roof.

An item that is still in use and functional for its intended purpose should not be depreciated beyond 90.

How to depreciate a new roof on rental property.

Complex irs regulations give owners of apartment buildings and other commercial structures two options when they dispose of a building s structural components such as a roof hvac unit or windows.

The most common and often significant item that is evaluated is roofing related work.

For example if the new roof costs 15 000 divide that figure by 27 5.

The roof depreciates in value 5 for every year or 25 in this case.

If a dwelling unit is used for personal purposes on a day it is rented at a fair rental price discussed earlier don t count that day as a day of rental use in applying 2 above.

They can either continue to depreciate the cost of the replaced component or they can fully deduct the unrecovered cost of the component in the year it is replaced.

10 of the total days it is rented to others at a fair rental price.

Are generally depreciated over a recovery period of 27 5 years using the straight line method of depreciation and a mid month convention as residential rental property.

See what is a day of personal use later.

Let s say your roof is supposed to last 20 years and it s 5 years old when damaged.

A capital improvement is any major replacement or renovation that betters the rental property or.

Repainting the exterior of your residential rental property.

Figure out the beginning and end dates.

The irs states that a new roof will depreciate over the course of 27 5 years for residential buildings and over the course of 39 years for commercial buildings.

In many cases only a portion of the roofing system is replaced and depending on the facts those costs may be deducted as repairs.

For example going from asphalt shingles 20 year life to clay tile 50 year life is a betterment that requires capitalization.

This means the roof depreciates 545 46 every year.